[ad_1]

Inventory Continues to Outpace 2024 Levels, Buyers Pay Less for Third Straight Month

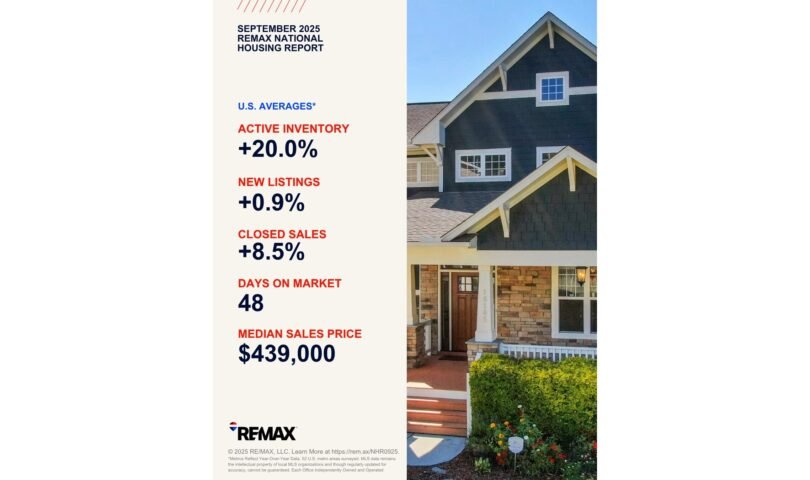

DENVER, Oct. 16, 2025 /PRNewswire/ — Inventory was 20% higher year-over-year – as September became the 21st consecutive month of annual growth. Home sales in September were 8.5% higher than a year ago, marking the fourth month in 2025 where sales outpaced the previous year. Compared to August, sales declined 4.6% while inventory rose 3.1% – typical shifts for this time of year.

Active inventory was up 20.0% year-over-year across the 52metro areas surveyed.

According to data from the 52 metro areas surveyed, buyers paid less for the third straight month as sellers accepted 98% of the asking price in September, down from 99% in both August 2025 and September 2024. The Median Sales Price in September was $439,000, a decrease of $6,000 (1.3%) from August but an increase of $9,000 (2.1%) compared to September 2024. This marked 27 consecutive months of year-over-year price gains. July’s median sales price of $450,000 was the highest recorded year to date.

Other metrics of note:

- Days on Market averaged 48 days, up one day from August and seven days from September 2024.

- Months’ Supply of Inventory rose to 3.0 months, up from 2.8 in August and 2.6 a year ago.

- New listings reversed a three-month decline and increased 4.5% over August and 0.9% year over year.

“Smart buyers are turning to their agents for strategic guidance – and it’s paying off, as many are still successfully negotiating favorable prices,” said REMAX CEO Erik Carlson. “At the same time, sellers can be confident in the continued demand for homes. As inventory grows and market dynamics shift, the months ahead may bring more balance to the market.”

While many markets experienced slightly lower median sales prices and longer days on market, Milwaukee, Wisconsin stood out in contrast, posting the largest year-over-year increase in median sales price (+11.5%) and ranked among the fastest-selling markets with an average of just 23 days on market.

|

Days on Market: |

|||

|

Market |

Sep 2025 |

Sep 2024 |

Year-over-Year |

|

Manchester, NH |

20 |

19 |

+8.1 % |

|

Milwaukee, WI |

23 |

22 |

+5.0 % |

|

Hartford, CT |

25 |

19 |

+34.9 % |

|

Omaha, NE |

27 |

26 |

+4.9 % |

|

Chicago, IL |

28 |

28 |

+0.7 % |

Dave Didier, Broker/Owner of three REMAX United offices in Milwaukee, says it continues to be a seller’s market there. “Inventory still isn’t where it needs to be for a balanced market here. Many would-be move-up buyers are staying put, deterred by higher home prices and mortgage rates that are double what they currently have. Instead, they’re choosing to renovate or expand. That’s keeping supply tight – but demand remains strong, especially from out-of-state buyers who see Milwaukee’s affordability, schools and quality of life as a major draw.”

Highlights and local market results for September include:

New Listings

In the 52 metro areas surveyed in September 2025, the number of newly listed homes was up 0.9% compared to September 2024, and up 4.5% compared to August 2025. The markets with the biggest year-over-year increase in new listings percentage were Omaha, NE at +20.9%, Fayetteville, AR at +20.1%, and Wichita, KS at +18.7%. The markets with the biggest decrease in year-over-year new listings percentage were Trenton, NJ at -38.3%, Dover, DE at -32.5%, and Baltimore, MD at -28.7%.

|

New Listings: |

|||

|

Market |

Sep 2025 |

Sep 2024 |

Year-over-Year |

|

Omaha, NE |

1,947 |

1,610 |

+20.9 % |

|

Fayetteville, AR |

1,263 |

1,052 |

+20.1 % |

|

Wichita, KS |

976 |

822 |

+18.7 % |

|

Indianapolis, IN |

3,486 |

3,048 |

+14.4 % |

|

Nashville, TN |

5,961 |

5,256 |

+13.4 % |

Closed Transactions

Of the 52 metro areas surveyed in September 2025, the overall number of home sales was up 8.5% compared to September 2024, and down 4.6% compared to August 2025. The markets with the biggest increase in year-over-year sales percentage were Honolulu, HI at +55.2%, Omaha, NE at +20.9%, and Raleigh, NC at +20.3%. The markets with the biggest decrease in year-over-year sales percentages were Dover, DE at -10.6%, Fayetteville, AR at -0.8%, and Indianapolis, IN at -0.3%.

|

Closed Transactions: |

|||

|

Market |

Sep 2025 |

Sep 2024 |

Year-over-Year |

|

Honolulu, HI |

931 |

600 |

+55.2 % |

|

Omaha, NE |

1,117 |

924 |

+20.9 % |

|

Raleigh, NC |

1,882 |

1,565 |

+20.3 % |

|

Wichita, KS |

795 |

675 |

+17.8 % |

|

Kansas City, MO |

2,697 |

2,292 |

+17.7 % |

Median Sales Price – Median of 52 metro area prices

In September 2025, the median of all 52 metro area sales prices was $439,000, up 2.1% from September 2024, and down 1.3% compared to August 2025. The markets with the biggest year-over-year increase in median sales price were Milwaukee, WI at +11.5%, Trenton, NJ at +10.6%, and Coeur d’Alene, ID at +9.2%. The markets with the biggest year-over-year decrease in median sales price were Houston, TX at -2.7%, Tampa, FL at -2.4%, and Honolulu, HI at -1.8%.

|

Median Sales Price: |

|||

|

Market |

Sep 2025 |

Sep 2024 |

Year-over-Year |

|

Milwaukee, WI |

$380,000 |

$340,825 |

+11.5 % |

|

Trenton, NJ |

$470,000 |

$425,000 |

+10.6 % |

|

Coeur d’Alene, ID |

$575,000 |

$526,500 |

+9.2 % |

|

Burlington, VT |

$480,000 |

$440,000 |

+9.1 % |

|

Providence, RI |

$520,000 |

$479,000 |

+8.6 % |

Close-to-List Price Ratio – Average of 52 metro area prices

In September 2025, the average close-to-list price ratio of all 52 metro areas in the report was 98%, down from 99% in both September 2024 and August 2025. The close-to-list price ratio is calculated by the average value of the sales price divided by the list price for each transaction. When the number is above 100%, the home closed for more than the list price. If it’s less than 100%, the home sold for less than the list price. The metro areas with the lowest close-to-list price ratios were Miami, FL at 94.1%, Bozeman, MT at 95.4%, and New Orleans, LA at 95.8%. The metro areas with the highest close-to-list price ratio were Hartford, CT at 102.9%, San Francisco, CA at 101.8%, and Manchester, NH at 101.0%.

|

Close-to-List Price Ratio: |

|||

|

Market |

Sep 2025 |

Sep 2024 |

Year-over-Year |

|

Miami, FL |

94.1 % |

94.1 % |

+0.0 pp |

|

Bozeman, MT |

95.4 % |

95.8 % |

-0.4 pp |

|

New Orleans, LA |

95.8 % |

95.8 % |

+0.0 pp |

|

Houston, TX |

96.4 % |

97.1 % |

-0.7 pp |

|

Tampa, FL |

96.5 % |

97.0 % |

-0.5 pp |

|

*Difference displayed as change in percentage points |

|||

Days on Market – Average of 52 metro areas

The average days on market for homes sold in September 2025 was 48, up seven days compared to the average in September 2024 and up one day compared to August 2025. The metro areas with the highest days on market averages were San Antonio, TX at 88, Miami, FL at 83 and Coeur d’Alene, ID at 77. The lowest days on market were Manchester, NH at 20, Milwaukee, WI at 23 and Hartford, CT at 25. Days on market is the number of days between when a home is first listed in an MLS and a sales contract is signed.

|

Days on Market: |

|||

|

Market |

Sep 2025 |

Sep 2024 |

Year-over-Year |

|

San Antonio, TX |

88 |

77 |

+15.0 % |

|

Miami, FL |

83 |

64 |

+29.1 % |

|

Coeur d’Alene, ID |

77 |

82 |

-6.4 % |

|

Bozeman, MT |

76 |

64 |

+18.6 % |

|

Phoenix, AZ |

74 |

60 |

+23.4 % |

Months’ Supply of Inventory – Average of 52 metro areas

The number of homes for sale in September 2025 was up 20.0% from September 2024, and up 3.1% from August 2025. Based on the rate of home sales in September 2025, the months’ supply of inventory was 3.0, up from 2.6 from September 2024, and up 2.8 from August 2025. In September 2025, the markets with the highest months’ supply of inventory were Miami, FL at 7.0, San Antonio, TX at 6.6 and Bozeman, MT at 5.4. The markets with the lowest months’ supply of inventory were Hartford CT at 1.2, Manchester, NH at 1.3 and Albuquerque, NM, Philadelphia, PA, Milwaukee, WI and Seattle, WA tied at 1.6.

|

Months’ Supply of Inventory: |

|||

|

Market |

Sep 2025 |

Sep 2024 |

Year-over-Year |

|

Miami, FL |

7.0 |

6.4 |

+7.8 % |

|

San Antonio, TX |

6.6 |

5.2 |

+28.0 % |

|

Bozeman, MT |

5.4 |

5.7 |

-5.1 % |

|

Houston, TX |

5.1 |

4.3 |

+19.6 % |

|

Atlanta, GA |

4.7 |

3.9 |

+20.5 % |

About the REMAX Network

As one of the leading global real estate franchisors, RE/MAX, LLC is a subsidiary of RE/MAX Holdings (NYSE: RMAX) with more than 145,000 agents in nearly 9,000 offices and a presence in more than 110 countries and territories. Nobody in the world sells more real estate than REMAX, as measured by residential transaction sides. REMAX was founded in 1973 by Dave and Gail Liniger, with an innovative, entrepreneurial culture affording its agents and franchisees the flexibility to operate their businesses with great independence. REMAX agents have lived, worked and served in their local communities for decades, raising millions of dollars every year for Children’s Miracle Network Hospitals® and other charities. To learn more about REMAX, to search home listings or find an agent in your community, please visit www.remax.com. For the latest news about REMAX, please visit news.remax.com.

Report Details

The REMAX National Housing Report is distributed monthly on or about the 15th. The Report is based on MLS data for the stated month in 52 metropolitan areas, includes single-family residential property types and is not annualized. For maximum representation, most of the largest metro areas in the country are represented, and an attempt is made to include at least one metro area in almost every state. Metro areas are defined by the Core Based Statistical Areas (CBSAs) established by the U.S. Office of Management and Budget.

Definitions

Closed Transactions are the total number of closed residential transactions during the given month. Months’ Supply of Inventory is the total number of residential properties listed for sale at the end of the month (current inventory) divided by the number of sales contracts signed (pending listings) during the month. Where “pending” data is unavailable, an inferred pending status is calculated using closed transactions. Days on Market is the average number of days that pass from the time a property is listed until the property goes under contract. Median Sales Price for a metro area is the median sales price for closed transactions in that metro area. The nationwide Median Sales Price is calculated at the nationwide aggregate level using all sale prices from the included metro areas. The Close-to-List Price Ratio is the average value of the sales price divided by the list price for each closed transaction.

MLS data is provided by Seventy3, LLC, a RE/MAX Holdings company. While MLS data is believed to be reliable, it cannot be guaranteed. MLS data is constantly being updated, making any analysis a snapshot at a particular time. Every month, the previous period’s data is updated to ensure accuracy over time. Raw data remains the intellectual property of each local MLS organization.

SOURCE RE/MAX, LLC

[ad_2]

Source link